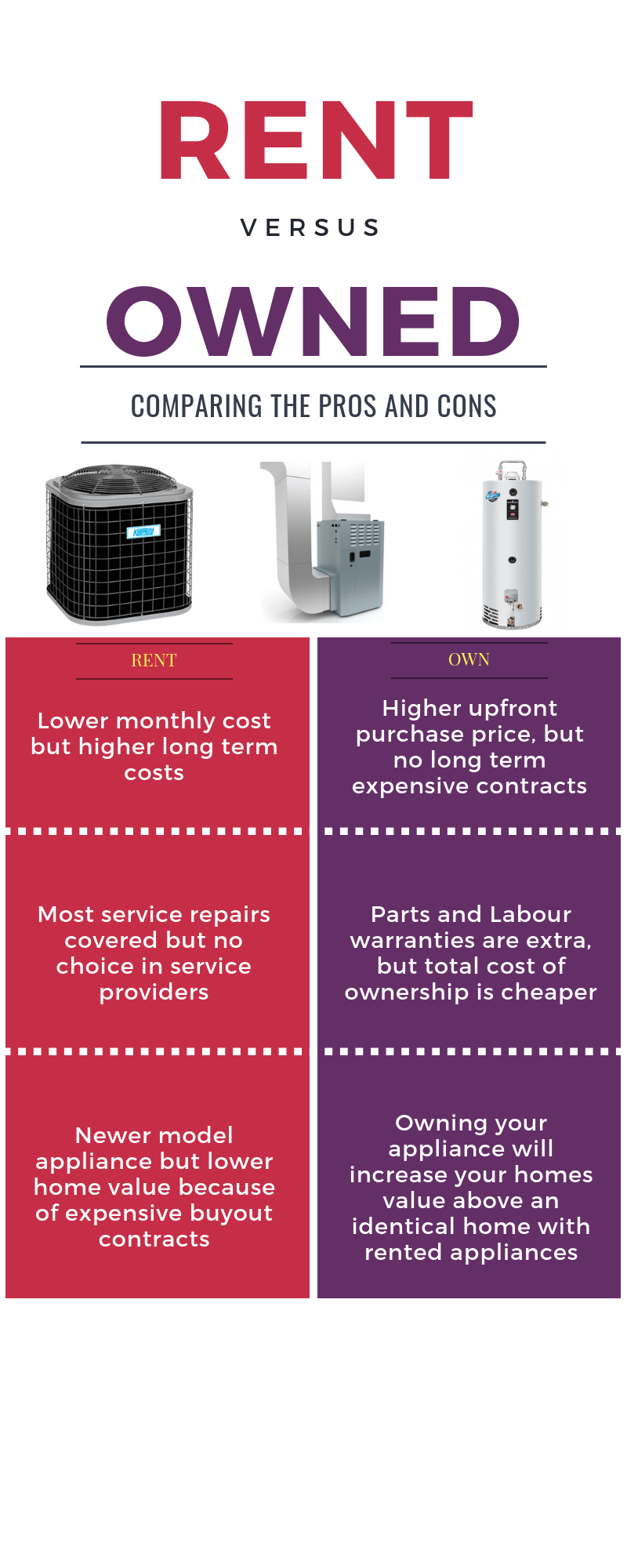

Understanding Closing Costs when Trading Real Estate

Preparing for the costs of associated with Real Estate Transactions

Closing Costs Associated with Real Estate Transactions.

Closing costs -‐ the list of charges that your lawyer presents to you on the closing date -‐ surprisesmany people because they are additional costs over and above the price of the home. According to CMHC, one should have, in addition to the down payment, at least 1.5% of the purchase price for closing costs (we say 2-‐2.5%, just to be on the safe side). The costs vary among provinces, and for that matter, among cities.

Below you will find a brief explanation of these costs. Please note that not all of them may apply to your specific situation, and there may be more that apply in your circumstance. Use this is a guideline, and then talk with your lawyer who can provide a more realistic estimate for your situation, since he or she is the best resource for your closing costs.

SELLER Vs BUYER

The seller is usually responsible for Real Estate Fees, Lawyer fees, new survey (if one can not be provided to the buyer).

The Buyer is usually responsible for home inspection, Appraisal (if the finance company requests it), home insurance, Lawyers fees, Land transfer Tax, and mortgage processing fees, CMHC fees if down payment is less than 25%

Description of Fees

Real Estate Fees: In Ontario, up to 5% of sale price plus HST.

Appraisal Fee: The appraisal provides the lenders with a professional opinion of the market value of the property. This cost is normally the borrower's responsibility and it ranges as low as $600 for a drive-‐by appraisal to as much as $1500 for a full appraisal, and the average being $800, plus H.S.T. Occasionally, the costs could be slightly higher for larger, custom-‐built homes, or homes in remote parts.

Home Inspection Fee: A professional inspection of the home, top to bottom, is for the benefit of the buyer, therefore, that's who absorbs the cost. A typical home inspection can cost anywhere from $300-‐$500, but our opinion is that they are well worth the investment. In highly competitive real estate markets, buyers may waive this clause, but we highly recommend doing a home inspection every time your purchase a home. When hiring a home inspector, make sure the inspector has liability insurance, just in case a mistake is made.

Home Insurance: All mortgage lenders will require a certificate of home insurance to be in place from the time you take possession of the home. The amount required is generally at least the amount of the mortgage or the replacement cost of the home. This cost can vary on the property size and extras being insured, as well as the insurance company and the municipality. The cost can vary anywhere from $600-$1500/year for most properties.

Harmonized Sales Tax (H.S.T.): If your mortgage is CMHC insured (less than 25% down payment), there is H.S.T. of 13% in Ontario, payable at closing, on the CMHC fee. While the insurance premium can be added to the mortgage amount, the H.S.T. must be paid at closing. For example, a mortgage that results in a $1,000 CMHC fee, will have to pay $130 in HST upon closing.

Land Survey Fee Or Title Insurance Fee: A recent Survey of the property is usually required by the lender, and if one is not available, it normally costs anywhere from $1000-‐$3000 for a new survey. In lieu of the Survey, most lenders today will accept Title Insurance, at a much lower price of approximately $250-$500.

Legal Costs and Disbursements: A lawyer or notary will charge a fee for their professional services involved in drafting the title deed, preparing the mortgage, and conducting the various searches. The disbursements, on the other hand, are out-‐of-‐pocket expenses incurred, such as registrations, searches, supplies, etc., plus H.S.T.

Land Transfer Tax: Most provinces charge a land transfer tax, payable by the purchaser, and the amount varies from province to province. This tax is based on the purchase price.

Current Land Transfer Tax Rates

- 0.5% of the value of consideration for the transfer up to and including $55,000,

- 1% of the value of the consideration which exceeds $55,000 up to and including

$250,000, and

- 1.5% of the value of the consideration which exceeds $250,000 and up to $400,000, and

- 2% of the balance up to $2 Million

- Greater than $2 Million is taxed at 2.5%

New Home Warranty: In many provinces, new homes are covered by a new home warranty program. The cost to the purchaser for this warranty is approximately $600 and should the builder default or fail to build to an agreed-‐upon standard, the fund will finish or repair the deficiencies.

Mortgage Application and Processing Fee: On a high-‐ratio insured mortgage (mortgages above 75% of the purchase price), the mortgage insurer (CMHC) charges a fee for applying and processing the file, as well as appraising the property. On new homes, this fee is less. Visit CMHC for up to date fee calculation.

Closing Adjustments: An estimate should be made for closing adjustments for bills that the seller has prepaid such as property taxes, utility bills, and other charges. Any bills after the closing date are the purchaser's responsibility. Your lawyer/notary will let you know what they are exactly once the various searches have been completed.

H.S.T.: On the purchase of a newly constructed home, HST is payable, but make sure you know who pays this, you or the builder. Therefore, on the offer, the purchase price will say "Plus HST" or "HST Included", and who gets the HST new home rebate. A lot of builders have included this cost into the purchase price so that the buyer does not have to come up with that at closing. (As well, this tax is also charged on all professional fees).

About the Author

Francesca Belle has been a Realtor® in Ontario since 2006. Her mission is to deliver a relaxed and refined buying and selling experience, and to operate with high standards of integrity, expertise and loyalty to her clients. Contact homes@francescabelle.com for all your real estate needs.

Share